Does the Sustained Global Demand for Oil, Gas and Minerals mean that Africa can now fund its Own MDG Financing Gap?

Keywords:

Economics, Economic growth, Private sector, sub-Saharan AfricaSynopsis

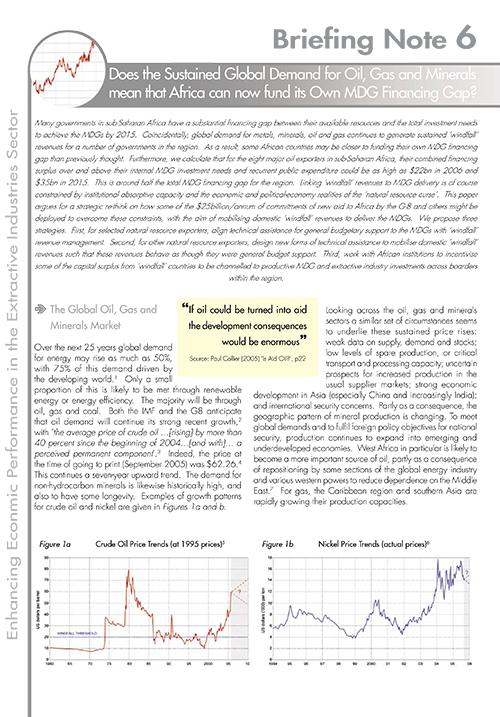

Many governments in sub-Saharan Africa have a substantial financing gap between their available resources and the total investment needs to achieve the MDGs by 2015. Coincidentally, global demand for metals, minerals, oil and gas continues to generate sustained 'windfall' revenues for a number of governments in the region. As a result, some African countries may be closer to funding their own MDG financing gap than previously thought. Furthermore, we calculate that for the eight major oil exporters in sub-Saharan Africa, their combined financing surplus over and above their internal MDG investment needs and recurrent public expenditure could be as high as $22bn in 2006 and $35bn in 2015. This is around half the total MDG financing gap for the region. Linking 'windfall' revenues to MDG delivery is of course constrained by institutional absorptive capacity and the economic and political-economy realities of the 'natural resource curse'. This paper argues for a strategic re-think on how some of the $25 billion/annum of commitments of new aid to Africa by the G-8 and others might be deployed to overcome these constraints, with the aim of mobilising domestic 'windfall' revenues to deliver the MDGs.

Downloads

Published

Series

Online ISSN

Categories

License

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.